In a striking development in India’s fiercely competitive two-wheeler market, February 2025 witnessed an intriguing divergence between wholesale and retail performance metrics. While Honda Motorcycle & Scooter India (HMSI) overtook Hero MotoCorp in monthly dispatches to dealers, Hero continued to maintain its leadership position in actual retail sales to end customers. This paradox highlights the complex dynamics of market share measurement in the automotive industry and reveals deeper strategic patterns in India’s two-wheeler landscape.

The Wholesale vs. Retail Paradox

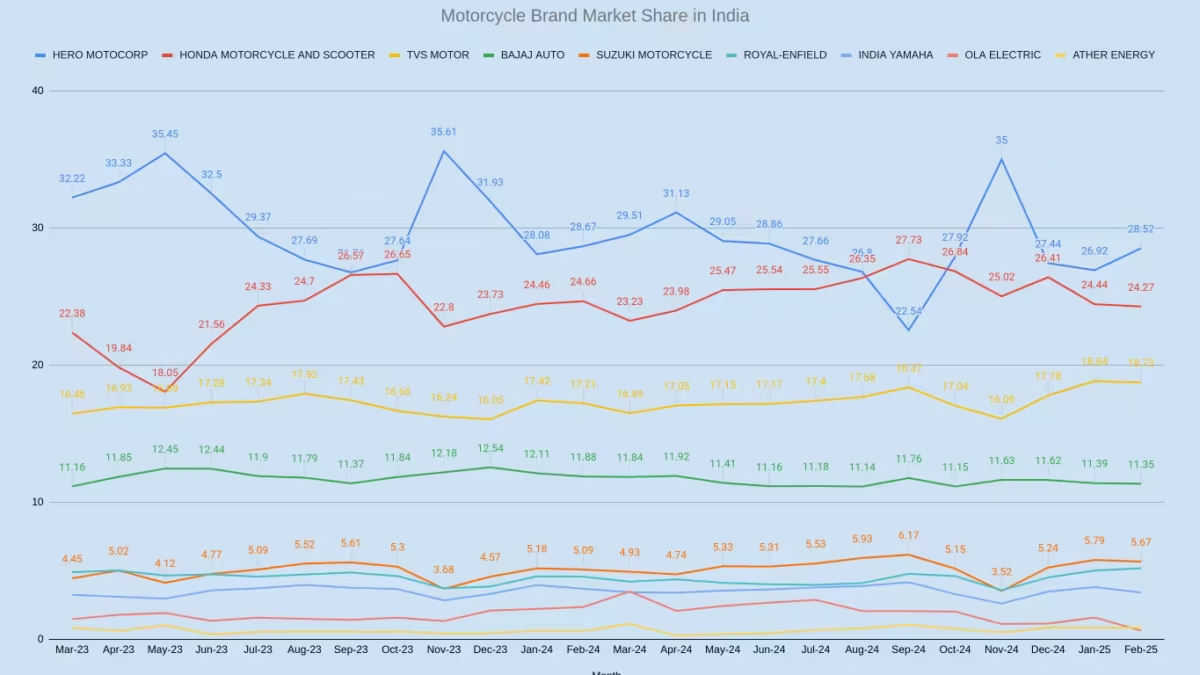

According to recent industry data, Honda dispatched 3.84 lakh two-wheelers to its dealer network in February, surpassing Hero MotoCorp’s 3.57 lakh units. This wholesale victory marks Honda’s third instance of outpacing Hero in monthly domestic dispatches this fiscal year, following similar achievements in July and August. However, FADA (Federation of Automobile Dealers Associations) retail data presents a different picture: Hero MotoCorp commanded a 28.52% retail market share in February 2025, significantly ahead of Honda’s 24.27%.

This 4.25 percentage point gap between the two giants in actual retail sales stands in stark contrast to Honda’s apparent dominance in wholesale numbers. The discrepancy underscores a fundamental industry reality – wholesale figures represent manufacturers’ shipments to dealers, while retail data reflects actual purchases by consumers.

Historical Trends: A Market in Flux

Examining the 24-month trend from March 2023 to February 2025 reveals a market characterized by both stability and subtle shifts. Hero MotoCorp has maintained its retail market leadership position throughout most of this period, albeit with considerable fluctuations ranging from 22.54% (September 2024) to 35.61% (November 2023).

Honda’s retail market share has followed a generally strengthening trajectory, growing from 22.38% in March 2023 to 24.27% in February 2025, with a notable peak of 27.73% in September 2024 – the only month when Honda briefly surpassed Hero in retail market share. This momentary leadership was short-lived, with Hero reclaiming its dominant position in the following months.

The data shows three distinct retail market share patterns:

Hero MotoCorp consistently demonstrates marked increases in market share during November (35.61% in 2023 and 35.00% in 2024), indicating potential seasonal advantages in rural markets during post-harvest periods. Despite occasional dips, Honda has shown a gradual strengthening trend, narrowing the retail gap with Hero from approximately 10 percentage points in early 2023 to about 4-5 points by early 2025. While the Hero-Honda dynamic dominates headlines, TVS Motor has quietly increased its retail market share from 16.46% in March 2023 to 18.73% in February 2025, positioning it as a strengthening third player.

The Strategy Behind the Numbers

The divergence between wholesale and retail performance reveals contrasting business strategies. Honda’s aggressive push in wholesale volumes suggests a determined effort to expand its dealer network’s inventory and market presence. This approach aligns with Minoru Kato’s recent statement that Honda is “well within reach of the largest market share in India.”

However, Hero’s continued retail leadership indicates stronger end-customer connections, particularly in its traditional strongholds. Industry analysts point to several factors maintaining Hero’s retail edge:

Hero’s extensive distribution network in rural India provides resilience against Honda’s urban-centric growth strategy. Despite weakening demand in the entry-level motorcycle segment (Hero’s traditional stronghold), the company maintains substantial customer loyalty in this category. Decades of market leadership have created strong brand recognition for Hero, particularly in non-metropolitan markets.

Meanwhile, Honda’s competitive gains stem primarily from:

The revival in scooter sales has disproportionately benefited Honda, whose Activa remains the segment leader. Models like the Shine 100 have helped Honda capture incremental volumes in the commuter motorcycle segment, traditionally Hero’s territory. Honda’s stronger presence in higher-margin segments has improved both profitability and brand perception.

Market Share Pressures and Responses

Hero MotoCorp’s market position has faced increasing pressure throughout the 2024-25 fiscal year. Its domestic market wholesale share declined to 28.6% during April-December 2024 from 30.2% in FY24. Simultaneously, Honda’s share improved to 27.2% from 25.2% during the same period.

The cumulative wholesale gap between the two companies has narrowed dramatically – standing at just 1.77 lakh units in the current financial year, down from 8.90 lakh units in the year-ago period. This rapid convergence suggests a structural shift in the market’s competitive dynamics.

Hero’s response has been multifaceted. The company has enhanced its premium segment offerings, accelerated its electric vehicle strategy with the Vida sub-brand, and intensified dealer support initiatives. These efforts appear to be maintaining Hero’s retail market advantage despite wholesale pressures.

The Broader Competitive Landscape

While the Hero-Honda battle captures headlines, the broader market shows other notable developments. TVS Motor has strengthened its position as a solid third player with consistently improving retail performance. Bajaj Auto maintains remarkable stability at around 11-12% retail market share, demonstrating resilience in a changing market.

The electric vehicle segment also continues to evolve, with Ola Electric and Ather Energy showing modest but persistent presence. Ola’s retail market share peaked at 3.49% in March 2024 but has subsequently settled at lower levels, highlighting the challenges of sustaining momentum in the EV space.

Future Outlook and Implications

The current divergence between wholesale and retail performance metrics suggests several potential future scenarios:

Honda’s aggressive wholesale push might lead to dealer inventory buildup, potentially necessitating corrections if retail performance doesn’t match wholesale volumes. Aware of the gap between wholesale and retail numbers, Honda will likely increase marketing and dealer incentives to convert higher inventories into actual sales. Hero MotoCorp may accelerate product launches and dealer support initiatives to maintain its retail edge while addressing wholesale volume challenges. The widening gap between wholesale and retail figures across the industry points to potential market rationalization if consumer demand doesn’t absorb increased dealer inventories.

February 2025’s contrasting wholesale and retail performance metrics highlight the nuanced reality of India’s two-wheeler market. While Honda’s wholesale victory represents a significant milestone in its challenge to Hero’s dominance, Hero MotoCorp’s continued retail leadership demonstrates the resilience of its market position.

The coming months will be crucial in determining whether Honda can translate its wholesale advantage into sustainable retail leadership. Meanwhile, Hero faces the challenge of defending its retail market share while addressing the wholesale volume gap with its primary competitor.

For industry observers, this situation underscores the importance of distinguishing between different market share metrics and understanding the strategic implications of each. In the battle for India’s two-wheeler market, both wholesale push and retail pull strategies play essential roles – and currently, these strategies are yielding divergent results for the industry’s two largest players.